Money Habits That Build Wealth After 40

If you’re a man over 40 wondering whether it’s too late to build real wealth, let me stop you right there. The wealth building habits for men over 40 aren’t just possible—they’re often more effective than starting younger because you have experience, wisdom, and (hopefully) fewer financial distractions.

“The habits you build today determine the wealth you’ll have tomorrow. It’s never too late to start building the right foundation.”

– Warren Buffett

The truth is, money habits after 40 can be your secret weapon. While younger guys are still figuring out what they want, you know what matters. You understand the value of time, and you’re ready to make moves that count. Let’s dive into the specific financial habits for success that can transform your financial future, regardless of where you’re starting.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Why Your 40s Are Prime Time for Wealth Building

Here’s something most financial advice gets wrong: your 40s aren’t the “catch-up” years—they’re the wealth acceleration years. You’ve got 20-25 years until traditional retirement, which is plenty of time for compound interest to work its magic. Plus, you likely have higher earning potential and better financial discipline than you did in your 20s.

The key is developing the right wealth building strategies that fit your life stage. No more gambling on risky investments or following get-rich-quick schemes. It’s time for proven, sustainable money management after 40 that builds lasting wealth.

The Foundation: Automate Your Wealth Building

1. Pay Yourself First (The Non-Negotiable 20%)

The most powerful wealth building habit is treating savings like a bill you can’t skip. Before rent, before groceries, before anything else—20% of your income goes to wealth building. If 20% feels impossible right now, start with 10% or even 5%. The habit matters more than the amount.

For different income levels:

- $50,000/year: Start with $200-400/month ($2,400-4,800/year)

- $75,000/year: Aim for $625-1,250/month ($7,500-15,000/year)

- $100,000+/year: Target $1,650+/month ($20,000+/year)

2. Set Up Wealth-Building Automation

Automation removes willpower from the equation.

Set up automatic transfers to:

- High-yield savings account (emergency fund)

- 401(k) or IRA (retirement)

- Investment account (wealth building)

- Debt payments (if applicable)

Think of automation like having a personal financial assistant who never takes a day off. Every payday, your money automatically flows where it needs to go before you even see it.

The Wealth Multipliers: Investment Habits That Compound

3. Master the Art of Consistent Investing

Dollar-cost averaging might sound fancy, but it’s simple: invest the same amount every month, regardless of market conditions. When prices are high, you buy fewer shares. When prices are low, you buy more. Over time, this smooths out market volatility.

Real Example: Investing $500/month in a broad market index fund. Some months you might buy shares at $100 each (5 shares), other months at $80 each (6.25 shares). Over 20 years, this consistency typically outperforms trying to time the market.

4. Diversify Your Income Streams

Passive income strategies become crucial after 40. You want money working for you while you sleep.

Start with:

- Dividend-paying stocks: Companies that pay you quarterly just for owning shares

- Real Estate Investment Trusts (REITs): Own real estate without being a landlord

- High-yield savings: Not exciting, but reliable and liquid

- Side hustles: Turn skills into income (The Side Hustle Bible has 100+ ideas)

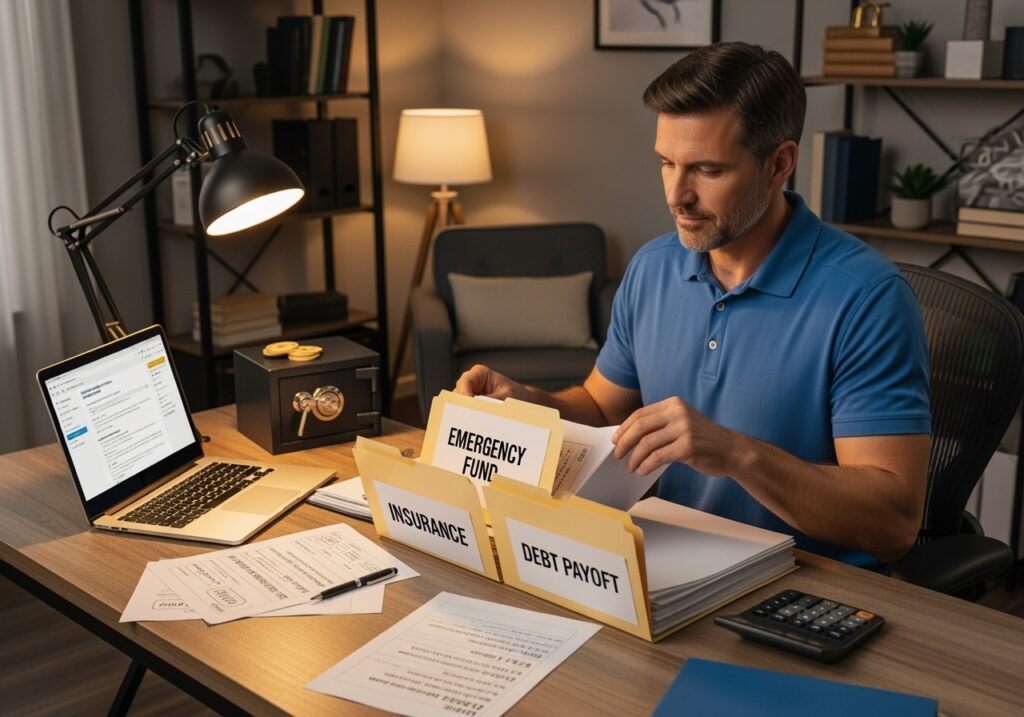

The Wealth Protectors: Smart Money Management

5. Build Your Financial Fortress (Emergency Fund)

An emergency fund isn’t just savings—it’s wealth protection. Without it, one car repair or medical bill can derail years of progress. Aim for 3-6 months of expenses, but start with $1,000 if that feels overwhelming.

Storage Strategy: Keep your emergency fund in a high-yield savings account that earns interest but remains easily accessible. Think of it as insurance for your wealth-building plan.

6. Eliminate High-Interest Debt Strategically

Not all debt is bad, but credit card debt averaging 18-24% interest will sabotage your wealth accumulation.

Use either:

Debt Snowball: Pay minimums on everything, attack smallest balance first (psychological wins)

Debt Avalanche: Pay minimums on everything, attack highest interest rate first (mathematical optimal)

Choose the method you’ll actually stick with. Consistency beats perfection.

The Wealth Accelerators: Advanced Habits

7. Optimize Your Tax Strategy

Tax optimization means keeping more of what you earn.

Max out tax-advantaged accounts first:

- 401(k): $23,000 limit (2024), plus $7,500 catch-up if 50+

- IRA: $7,000 limit, plus $1,000 catch-up if 50+

- HSA: $4,300 individual/$8,550 family (triple tax advantage)

Simple explanation: These accounts either reduce your taxes now (traditional) or eliminate taxes later (Roth). Either way, you keep more money.

8. Invest in Your Earning Power

The best investment after 40 might be yourself.

Skills that increase your income have unlimited returns:

- Professional certifications

- Industry conferences

- Online courses

- Networking events

Budget allocation: Invest 3-5% of your income in learning and development.

The Psychology of Wealth Building After 40

9. Develop a Wealth Mindset

Your money mindset determines your financial ceiling. Common limiting beliefs after 40:

- “It’s too late to start”

- “I should have started earlier”

- “Rich people are lucky/greedy”

- “I’m not good with money”

Replace these with wealth-building thoughts:

- “Every day is a new opportunity”

- “Experience gives me an advantage”

- “Wealthy people solve problems”

- “I can learn money management”

Related Article

Dive deeper into mindset transformation:

10. Track Your Progress Like a Pro

What gets measured gets managed.

Track:

- Net worth monthly (assets minus debts)

- Savings rate (percentage of income saved)

- Investment returns (but don’t obsess over short-term fluctuations)

- Debt reduction progress

Making It Work for Your Income Level

If You’re Earning $40,000-60,000:

- Focus on emergency fund first ($3,000-5,000)

- Maximize any employer 401(k) match

- Start with low-cost index funds ($50-100/month)

- Consider a side hustle for extra income diversification

If You’re Earning $60,000-100,000:

- Build larger emergency fund ($15,000-25,000)

- Max out 401(k) employer match, then Roth IRA

- Invest $500-1,000/month in diversified portfolio

- Explore real estate investment options

If You’re Earning $100,000+:

- Max out all tax-advantaged accounts

- Consider taxable investment accounts

- Explore advanced strategies (backdoor Roth, mega backdoor Roth)

- Work with a fee-only financial planner

The 90-Day Wealth Habit Challenge

Ready to start?

Here’s your financial transformation after 40 roadmap:

Days 1-30: Foundation

- Set up automatic savings (start with 5-10%)

- Open high-yield savings account

- Calculate your net worth baseline

- Read one wealth-building book

Days 31-60: Acceleration

- Increase savings rate by 2-5%

- Open investment account

- Start dollar-cost averaging

- Eliminate one unnecessary expense

Days 61-90: Optimization

- Review and optimize all accounts

- Increase 401(k) contribution

- Plan next quarter’s financial goals

- Celebrate your progress

Your Wealth Building Action Plan

The compound effect of good habits means small, consistent actions create massive results over time.

Here’s your immediate action plan:

- This week: Set up automatic savings transfer

- This month: Open investment account and make first investment

- Next 90 days: Build emergency fund to $1,000 minimum

- This year: Increase savings rate to 15-20%

Remember, wealth building habits that actually work aren’t complicated—they’re consistent. You don’t need to be perfect; you need to be persistent.

The Bottom Line

Building wealth after 40 isn’t about making up for lost time—it’s about making the most of the time you have. The proven financial habits for midlife success are simple: automate your savings, invest consistently, protect your wealth, and stay the course.

“Wealth is not about having a lot of money; it’s about having a lot of options. And those options come from the habits you build today.”

– Chris Hogan

Your 40s can be your most financially productive decade if you develop the right money habit stacking system. Start with one habit, master it, then add another. Before you know it, you’ll have built a wealth mindset and system that works automatically.

The best time to plant a tree was 20 years ago. The second-best time is today. Your future wealthy self is counting on the decisions you make right now.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Important Note: The information provided in this article is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making significant financial decisions. Your situation is unique, and these general guidelines may need to be adjusted to your specific circumstances.