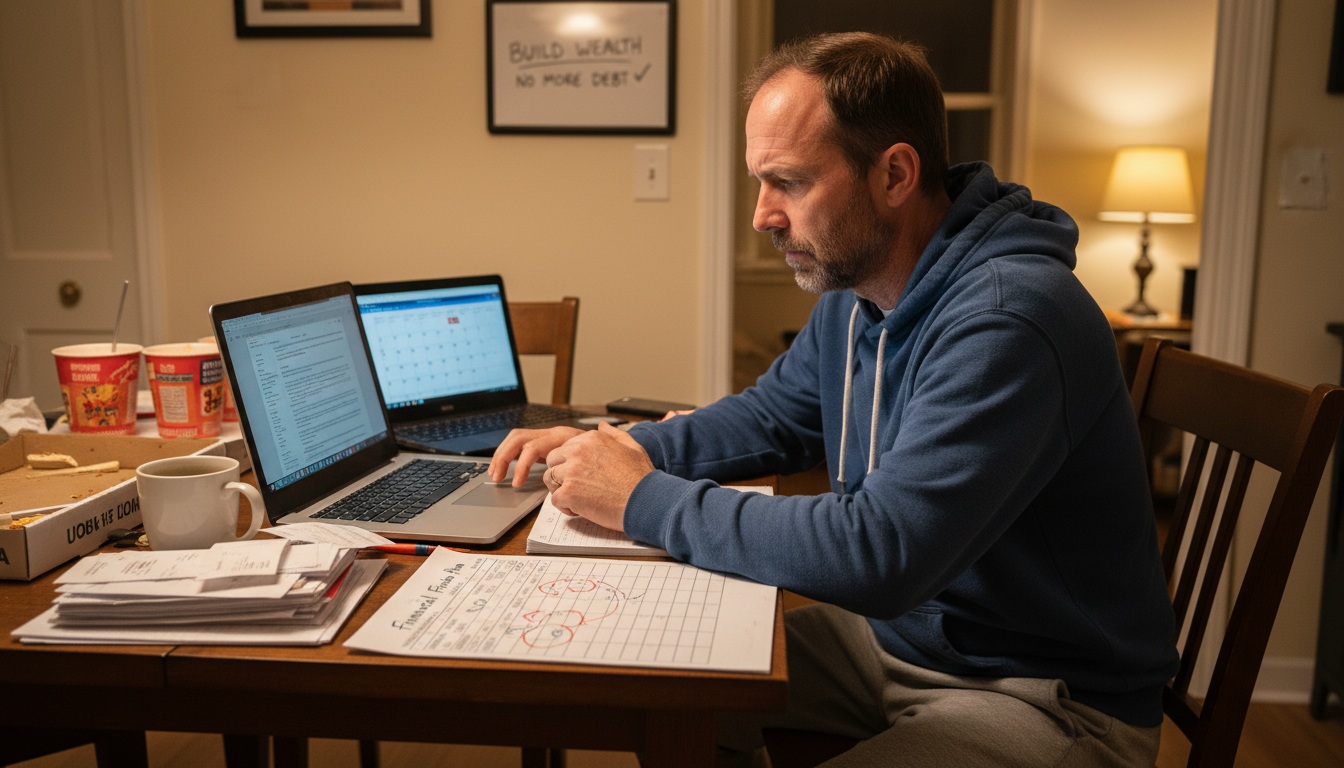

Q3 Financial Wrap-Up: Preparing for a Strong Q4 Finish

Here we are, gentlemen—three quarters through another year. If you’re like most men over 40, you’re probably wondering where the time went and whether your money situation is any better than it was in January. Don’t worry, you’re not alone in feeling like your finances might need some serious attention.

“The best time to plant a tree was 20 years ago. The second best time is now

– Chinese Proverb

This Q3 financial review for men over 40 isn’t about making you feel guilty about past money mistakes. It’s about giving you a practical, no-nonsense quarterly money check that’ll help you finish the year strong. Think of it as a financial health checkup—something every guy should do but most of us avoid like a trip to the dentist.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Why Your Q3 Financial Review Matters More Than You Think

Look, we get it. Financial wrap-ups sound about as exciting as watching paint dry. But here’s the thing—men who regularly review their finances are 3x more likely to reach their money goals than those who just “wing it.” Whether you’re making $35,000 as a restaurant manager or $85,000 as an engineer, this process works.

A quarterly financial checkup is simply looking at your money situation every three months. It’s like checking your car’s oil—ignore it too long, and you’ll end up broken down on the side of the road.

The Reality Check: Where You Stand Right Now

Before we dive into Q4 financial planning, let’s get brutally honest about where you are today. Grab a coffee, find a quiet spot, and let’s do this financial reality check together.

Your Income Assessment (The Good News First)

Start with the positive—what money came in during Q3?

- Primary job income: Your regular paycheck (after taxes)

- Side hustle performance: Any extra income from freelancing, part-time work, or that weekend gig

- Investment gains: Dividends, interest, or any profits from investments you sold

- Other income: Tax refunds, bonuses, gifts, or that $20 you found in your old jacket

Related Article

For more foundational strategies on building wealth in your 40s and beyond, check out our comprehensive guide: The Mid-Life Wealth Building Blueprint.

The Expense Analysis (Where Reality Hits)

Now for the part most of us dread—where did all that money go?

Your expense analysis should cover:

- Fixed expenses: Rent/mortgage, car payments, insurance, utilities

- Variable expenses: Groceries, gas, entertainment, that streaming service you forgot you had

- Unexpected costs: Car repairs, medical bills, or when your teenager needed “emergency” money

Don’t beat yourself up if the numbers don’t look pretty. Every guy I know has had months where money seemed to evaporate. The key is learning from it.

Your Q3 Financial Scorecard

Let’s break down your quarterly budget review into manageable pieces. Think of this as your financial report card—no judgment, just facts.

Cash Flow Check (Money In vs. Money Out)

Cash flow is simply money coming in minus money going out each month. If you’re consistently spending more than you earn, you’re in what we call “financial quicksand”—the longer you stay there, the deeper you sink.

For Q3, calculate:

- Total income for July, August, and September

- Total expenses for the same period

- The difference (positive means you’re ahead, negative means you’re behind)

If you need help organizing these numbers, “The Total Money Makeover” by Dave Ramsey provides excellent worksheets and step-by-step guidance for men who want to take control of their finances.

Debt Paydown Progress

Your debt-to-income ratio is how much of your monthly income goes toward paying debts (credit cards, loans, etc.). A healthy ratio is below 36%, but don’t panic if yours is higher—we can fix this.

Compare your debt levels from June to September:

- Credit card balances

- Personal loans

- Car loans

- Any other debts

Did they go up, down, or stay the same? Even a $100 reduction is progress worth celebrating.

Emergency Fund Status

Your emergency fund is money saved for unexpected expenses—think job loss, major car repairs, or medical bills. Financial experts recommend 3-6 months of expenses, but if you’re starting from zero, even $500 is a huge win.

Where does your emergency fund stand compared to three months ago? If it’s non-existent, don’t worry—we’ll fix that in your Q4 plan.

Learning From Your Q3 Money Mistakes

Here’s where we get real about those financial mistakes we all make. We’re not talking about beating yourself up—we’re talking about honest reflection so you don’t repeat the same patterns.

Common Q3 Financial Traps for Men Over 40

Summer spending sprees

Vacations, outdoor gear, or “treating the family”

Back-to-school expenses

Kids’ supplies, clothes, activities that add up fast

Home improvement projects

That deck repair that somehow cost three times the estimate

Impulse purchases

The gadget, tool, or hobby equipment you “needed”

The goal isn’t perfection—it’s awareness. When you understand your spending triggers, you can plan for them.

Your Q4 Financial Game Plan

Now for the good stuff—your Q4 financial preparation strategy. This isn’t about dramatic changes that’ll last two weeks. This is about sustainable money habits that’ll carry you into next year stronger than ever.

Set Realistic Q4 Financial Goals

Your Q4 financial goals should be specific and achievable.

Here are examples based on different income levels:

If you earn $30,000-$45,000 annually:

- Build a $300 emergency fund by December 31st

- Pay off one small debt completely

- Track every expense for the next 90 days

If you earn $45,000-$70,000 annually:

- Increase emergency fund by $750

- Boost retirement contribution by 1%

- Pay extra $50/month toward highest interest debt

If you earn $70,000+ annually:

- Maximize one tax-advantaged account (401k, IRA, HSA)

- Build emergency fund to cover 2 months of expenses

- Research one new investment opportunity

Budget Adjustments That Actually Work

Your budget adjustments for Q4 should focus on small, sustainable changes:

- The 1% rule: Reduce spending in one category by just 1% each month

- Automate everything: Set up automatic transfers to savings and debt payments

- Use the envelope method: Allocate cash for discretionary spending categories

Wealth Building Strategies for the Final Quarter

Your wealth building focus for Q4 should be simple but effective:

- Increase your income: Ask for that raise, start a side hustle, or sell stuff you don’t need

- Optimize your investments: Review your 401k allocation, consider low-cost index funds

- Reduce unnecessary expenses: Cancel subscriptions you don’t use, negotiate bills

For investment education that doesn’t require a finance degree, “The Simple Path to Wealth” by JL Collins is excellent. It explains investing in terms any guy can understand, regardless of background.

Here are practical tools for your financial goal tracking:

Digital Tools

- Mint: Free budgeting app that connects to your bank accounts

- Personal Capital: Great for tracking investments and net worth

- YNAB: Best for hands-on budgeting and breaking the paycheck-to-paycheck cycle

Old-School Methods

- Spreadsheet tracking: Simple Excel or Google Sheets templates

- Physical budget planners: For guys who prefer writing things down

- Weekly money meetings: 15 minutes every Sunday to review the week

The Budget Planner & Financial Organizer is perfect for men who want a comprehensive physical system for tracking income, expenses, and goals.

Note: Prices and availability may vary. Always check current Amazon pricing and read recent reviews before purchasing.

Common Q4 Financial Pitfalls to Avoid

As we head into the final quarter, watch out for these financial discipline killers:

Holiday overspending

Start planning now for gift expenses

Year-end splurges

“I deserve this” purchases that derail progress

Tax procrastination

Waiting until April to think about tax strategies

Investment panic

Making emotional decisions based on market volatility

Your 90-Day Action Plan

Here’s your practical quarterly assessment turned into action:

October (Month 1): Foundation Building

- Complete your Q3 financial review using this guide

- Set up automatic savings transfers

- Choose one debt to focus on paying down

- Start tracking daily expenses

November (Month 2): Momentum Building

- Review and adjust your budget based on October results

- Increase your emergency fund contribution

- Research holiday spending limits

- Consider year-end tax strategies

December (Month 3): Strong Finish

- Stick to your holiday spending plan

- Make any final retirement contributions

- Plan your Q1 financial goals

- Celebrate your progress (within budget!)

Related Article

For ongoing motivation and practical strategies, our article on Creating Multiple Income Streams After 40 provides excellent guidance on building financial independence after 40.

The Bottom Line: It’s Never Too Late

Your Q3 financial review for men over 40 isn’t about perfection—it’s about progress. Whether you discovered you’re doing better than you thought or realized you need to make some changes, the fact that you’re taking this step puts you ahead of most guys your age.

“You don’t have to be great to get started, but you have to get started to be great.”

– Les Brown

Remember, financial independence isn’t about having millions in the bank. It’s about having enough money to make choices based on what you want, not what you can afford. Every small step you take in Q4 gets you closer to that freedom.

Your money mindset matters more than your current bank balance. The habits you build in the next 90 days will determine whether next year’s financial review shows real progress or more of the same struggles.

Taking Action Today

Don’t let this be another article you read and forget. Pick one action from this Q4 financial planning guide and do it today:

- Calculate your Q3 cash flow

- Set up an automatic transfer to savings

- List your debts from smallest to largest

- Download a budgeting app

- Order one of the recommended books

The difference between men who build wealth and those who struggle isn’t intelligence, luck, or starting salary—it’s consistent action. Your future self will thank you for the steps you take today.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Important Note: The information provided in this article is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making significant financial decisions. Your situation is unique, and these general guidelines may need to be adjusted to your specific circumstances.