Summer Spending Traps: Protecting Your Financial Goals

Summer’s here, and with it comes a dangerous cocktail of vacation dreams, activity-packed weekends, and the irresistible urge to live it up. But here’s the reality check: summer can be a financial goal killer if you’re not careful. Those “harmless” summer spending traps can derail months of hard work faster than you can say “beach vacation.”

“A budget is telling your money where to go instead of wondering where it went.”

– Dave Ramsey

Don’t worry – We’re not here to tell you to lock yourself indoors until September. Instead, let’s talk about how to enjoy your summer while keeping your financial goals intact. Think of this as your financial sunscreen – protection that lets you enjoy the season without getting burned.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

The Vacation Budgeting Blueprint

Step 1: Set Your Vacation Budget Reality

Before you start dreaming about that perfect getaway, get real about what you can afford. A good rule of thumb is that your vacation shouldn’t cost more than 5-10% of your annual income.

Action steps:

- Calculate your total available vacation funds

- Include ALL costs: travel, lodging, food, activities, souvenirs

- Add a 20% buffer for unexpected expenses

- If the numbers don’t work, scale back or save longer

Pro Tip: Keep a Vacation Budget Planner & Travel Journal handy to organize all your trip finances in one place. These planners help you track expenses before, during, and after your trip, making it easier to stay within budget and learn from each vacation experience.

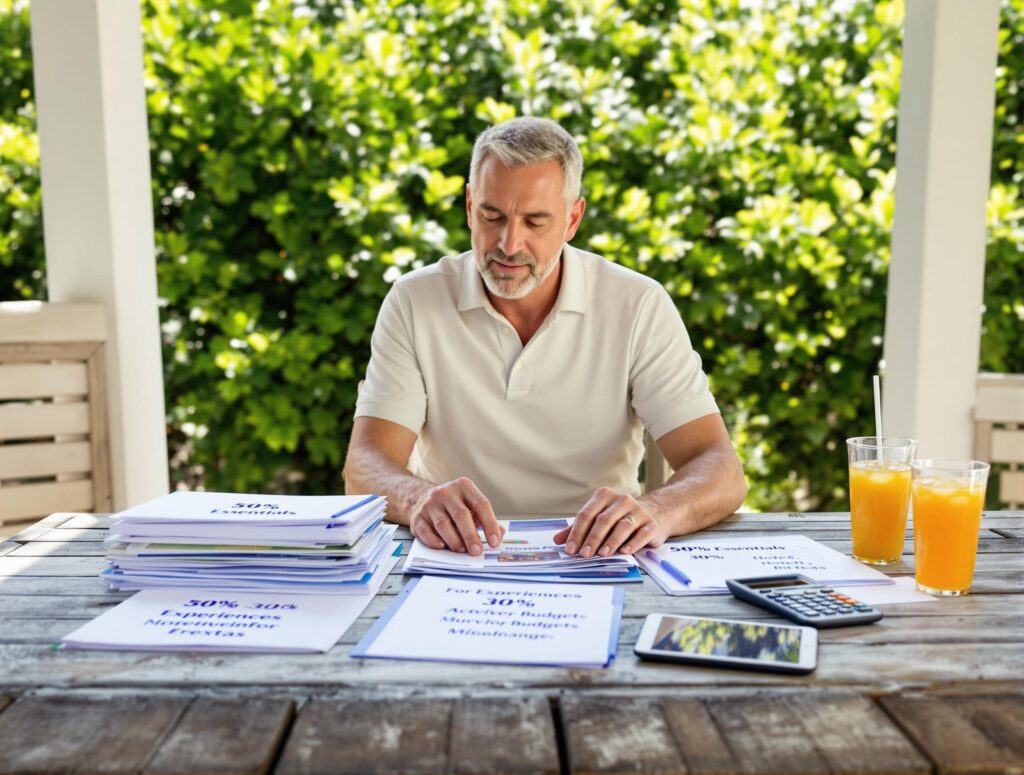

Step 2: Use the 50/30/20 Vacation Rule

Break your vacation budget into categories:

- 50% for essentials (flights, hotel, transportation)

- 30% for experiences (activities, tours, entertainment)

- 20% for extras (souvenirs, unexpected opportunities)

This rule prevents overspending in any one area and ensures you have money for the experiences that matter most. It’s part of building the triangle of well-being where financial health supports your overall life satisfaction.

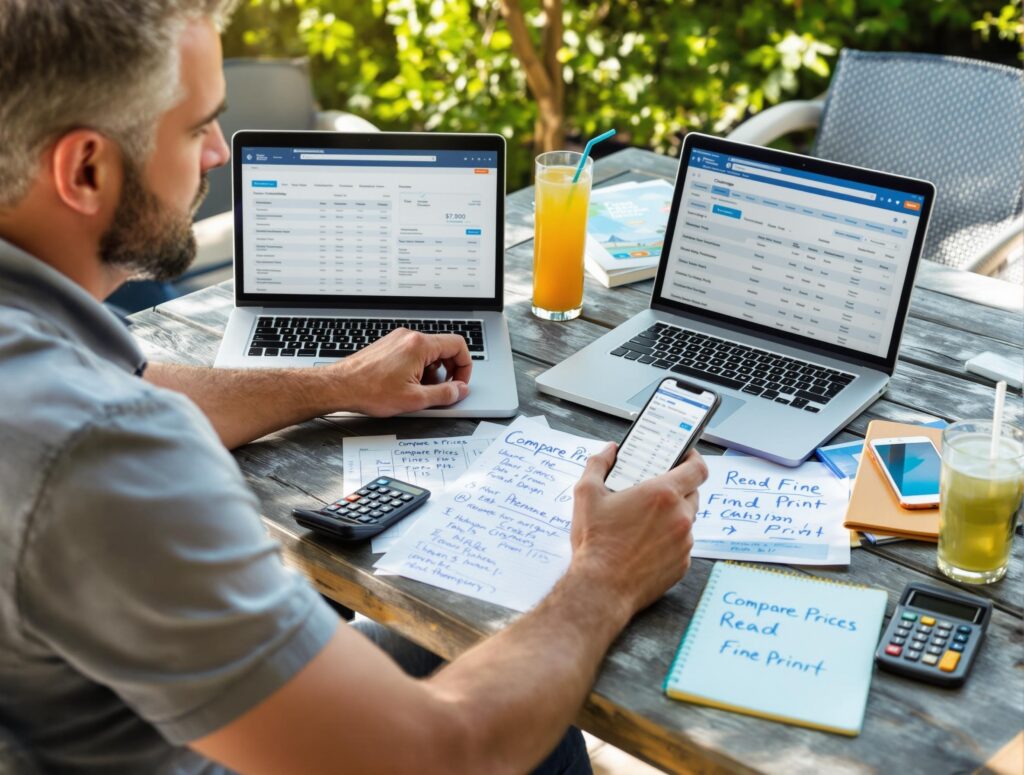

Step 3: Book Smart, Not Fast

Impulse booking is a major summer spending trap. Instead:

- Compare prices across multiple platforms

- Consider off-peak travel dates

- Look for package deals that actually save money

- Read the fine print for hidden fees

Common Challenges & Solutions for Men Over 40

Starting & Maintaining Exercise Routines

The Problem:

Many men in their 40s struggle with getting back into fitness, often making the mistake of doing too much too soon, leading to burnout or injury.

The Solution:

- Start with the “Foundation Five” approach – focus on 5 basic movements (squats, push-ups, planks, walking, stretching)

- Begin with just 10-15 minutes daily rather than hour-long workouts

- Implement morning mobility routines to build consistency

- Track progress weekly, not daily, to avoid obsessing over short-term fluctuations

Breaking Negative Self-Talk & Overthinking

The Problem:

Internal obstacles like negative mindset and overthinking prevent progress more than external circumstances.

The Solution:

- Use the “Clarity Framework” – write down specific concerns instead of letting them swirl in your head

- Practice basic meditation (even 5 minutes daily) to create mental space

- Implement the “24-hour rule” for major decisions to reduce impulsive overthinking

- Step out of your comfort zone with small, manageable actions rather than waiting for perfect conditions

Money Management & Changing Established Habits

The Problem:

Lack of understanding in money management makes it difficult to change long-established financial habits, especially when facing increased responsibilities.

The Solution:

- Start with a simple “Money Checklist” – track income, expenses, and one financial goal

- Focus on building one passive income stream rather than trying multiple approaches

- Use the “cost per use” formula before major purchases

- Automate savings and investments to remove decision fatigue from the equation

Balancing All Life Areas Without Overwhelm

The Problem:

Trying to improve physical health, mental resilience, and financial independence simultaneously can feel overwhelming and lead to abandoning all efforts.

The Solution:

- Apply the “Wellness Triangle” approach – focus on one pillar each month while maintaining basics in the others

- Build “Foundation Habits” that support multiple areas (like morning routines that include movement, mindfulness, and financial check-ins)

- Use holistic problem-solving by asking: “How does this decision affect my physical, mental, and financial well-being?”

- Start with integration rather than perfection – small improvements across all areas beat major progress in just one

Key Takeaway:

The biggest obstacle isn’t external circumstances – it’s the internal resistance to taking action. Start small, be consistent, and focus on building sustainable systems rather than seeking perfect solutions.

Managing Activity Costs Without Missing Out

Summer activities can drain your wallet faster than a leaky pool. Here’s how to stay active without breaking the bank:

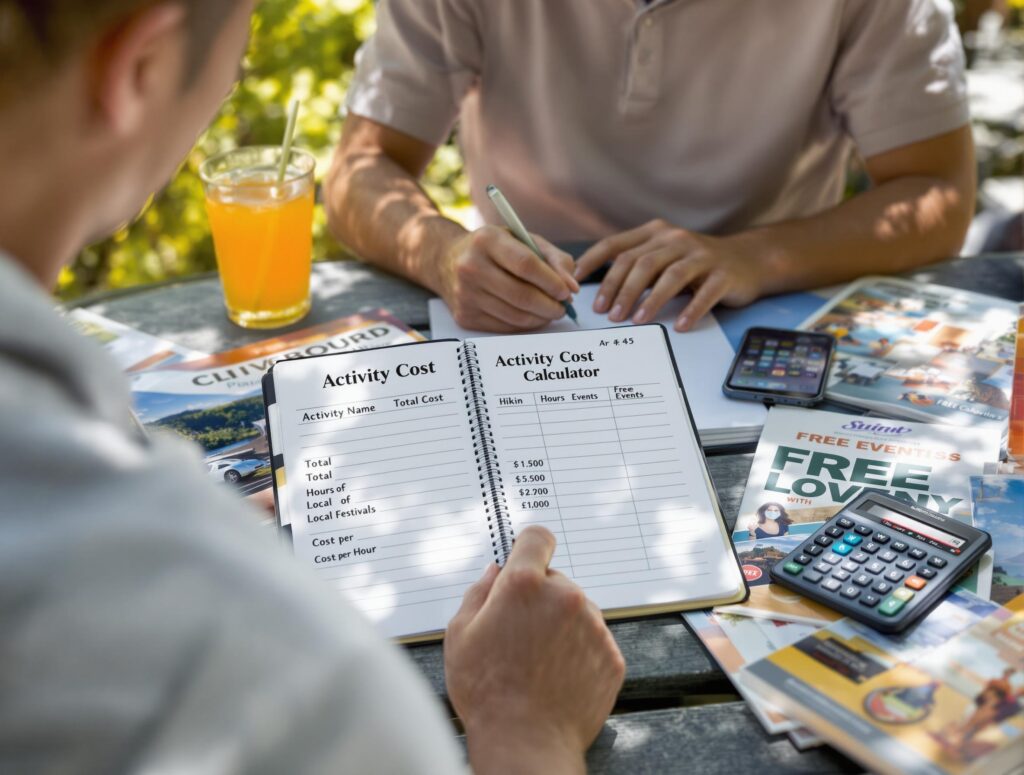

The Activity Cost Calculator Method

Before saying yes to any activity, run it through this quick calculation:

- Cost per hour: Divide total cost by hours of enjoyment

- Value assessment: Rate the experience importance (1-10)

- Budget impact: What percentage of your monthly fun money does this represent?

Keep a small pocket expense notebook with you to jot down potential activities and their costs. Writing things down helps you think more clearly about whether something is truly worth the expense. Sometimes seeing the numbers on paper is all it takes to make a smarter choice.

Smart Activity Swaps

This approach aligns perfectly with building mental toughness – it’s about making conscious choices rather than defaulting to expensive options.

The “One Splurge” Rule

Choose ONE big-ticket activity per month that you’re truly excited about, then find budget-friendly alternatives for everything else. This way, you get your highlight experience without the financial hangover.

Smart Spending Strategies for Summer Success

Strategy 1: The Summer Spending Account

Set up a separate savings account specifically for summer expenses. Transfer a set amount each month starting in spring. This prevents summer costs from blindsiding your regular budget.

Strategy 2: The 24-Hour Rule

For any non-essential purchase over $50, wait 24 hours before buying. You’ll be amazed how many “must-haves” lose their appeal after a day of reflection.

Consider keeping a decision journal where you write down items you’re considering buying. Include the price, why you want it, and how it fits into your budget. After 24 hours, review your entry. This simple practice can save you hundreds of dollars over a summer.

Strategy 3: Track Everything

Use a simple app or expense tracking journal to monitor every summer-related expense. Awareness is the first step to control. When you see where your money’s actually going, you can make better decisions.

Whether you prefer digital tracking or old-school pen and paper, the key is consistency. Many people find that physical tracking journals create more awareness than apps because the act of writing engages your brain differently.

Money-Saving Tips That Actually Work

Tip 1: Embrace the Power of “Free”

Every community has free summer activities – you just need to find them:

- Free outdoor movie screenings

- Community pool days

- Hiking trails and nature walks

- Library summer programs

- Local festivals and farmers markets

Tip 2: Master the Art of Potluck Planning

Instead of expensive restaurant gatherings, organize potluck barbecues and picnics. Everyone contributes, costs are shared, and the social experience is often better than eating out.

Invest in quality meal prep containers and a good cooler that will last for years. These tools make potluck planning easier and more enjoyable, while saving money on dining out throughout the summer.

Tip 3: Use the “Cost Per Use” Formula

Before buying summer gear, calculate cost per use. That $200 paddleboard might seem expensive, but if you use it 20 times over the summer, it’s only $10 per use – cheaper than renting.

When buying outdoor gear, focus on quality items that will last multiple seasons. Research reviews thoroughly and consider versatile pieces that serve multiple purposes. A good camping chair that works for beach days, concerts, and backyard gatherings is better than three specialized items.

Tip 4: Shop Your Own Closet First

Before buying new summer clothes or gear, thoroughly check what you already own. You might rediscover items that work perfectly for your summer plans.

This connects to the over-40 body reset philosophy – sometimes the best investment in your health and finances is making better use of what you already have rather than constantly acquiring new things.

Building Your Financial Knowledge Base

Smart summer spending isn’t just about tactics – it’s about developing the right financial mindset and knowledge. Here are some books that will transform how you think about money and spending:

Learn how to build lasting money-saving habits that stick beyond summer.

A step-by-step plan for financial fitness.

Understand why protecting your money today builds tomorrow's freedom.

A step-by-step plan for financial fitness.

Simple, actionable financial advice without overwhelming complexity.

Learn the spending habits of people who actually build wealth.

These books aren’t just summer reading – they’re investments in your financial education that will pay dividends for years to come.

Protecting Your Long-Term Financial Goals

Summer spending traps are particularly dangerous because they can derail your bigger financial picture.

Here’s how to maintain perspective:

The Goal Reminder System

Write down your top 3 financial goals and their deadlines. Before any significant summer purchase, ask: “Does this move me closer to or further from my goals?”

This ties directly into creating multiple income streams after 40 – every dollar you save from smart spending is a dollar that can be invested in building additional income sources.

The Opportunity Cost Question

For every dollar you spend on summer activities, ask what else that money could do. Could it go toward your emergency fund, debt payoff, or retirement savings? Sometimes the answer is still “enjoy summer,” but at least you’re making a conscious choice.

The Future Self Check

Imagine yourself in December looking back at your summer spending. Will you be proud of your choices, or will you wish you’d been more disciplined? This perspective can be a powerful decision-making tool.

Building this kind of long-term thinking is part of developing mental toughness in your prime years – it’s about making decisions based on your future self’s best interests, not just immediate gratification.

Your Summer Financial Action Plan

Week 1: Assessment and Planning

- Review your current financial situation

- Set your summer spending limits

- Create your vacation budget (if applicable)

- Set up your summer spending tracking system

- Get equipped: Order a vacation budget planner and expense tracking journal

Week 2: Research and Prepare

- Research free and low-cost activities in your area

- Compare prices for any planned purchases

- Set up your separate summer spending account

- Start reading: Pick one of the recommended financial books to begin building better money habits

Week 3: Implementation

- Start tracking all summer-related expenses

- Begin using the 24-hour rule for purchases

- Plan your first budget-friendly summer activity

- Invest in tools: Get quality reusable water bottles and picnic gear for budget-friendly outdoor activities

Week 4: Review and Adjust

- Assess your first week of summer spending

- Adjust your strategies based on what’s working

- Celebrate your smart financial choices

- Plan ahead: Research and bookmark free summer activities for the coming weeks

Getting Started: Your First Step

The best time to protect your financial goals was yesterday. The second-best time is right now. Start by choosing just ONE strategy from this post and implementing it this week.

Whether it’s setting up expense tracking, ordering a budget planner, or picking up one of the recommended books, taking action is what matters.

Consider starting with “The Index Card” by Helaine Olen – it’s a quick read that will give you a solid foundation for all the strategies in this post. Pair it with a simple expense tracking notebook, and you’ll have both the knowledge and tools to protect your financial goals this summer.

Final Thoughts

Remember, protecting your financial goals during summer isn’t about depriving yourself – it’s about making intentional choices that let you enjoy the season without sacrificing your future. This approach supports the triangle of well-being by ensuring your financial health enhances rather than undermines your overall life satisfaction.

“The real measure of your wealth is how much you’d be worth if you lost all your money.”

– Anonymous

Summer will come and go, but the financial habits you build and the goals you protect will serve you for years to come. Make this summer the one where you prove you can have fun AND stay financially responsible.

The tools, books, and strategies outlined in this post aren’t just about surviving summer spending – they’re about building a foundation for long-term financial success. Start with one small step today, and by the end of summer, you’ll have both great memories and a stronger financial position.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Important Note: The information provided in this article is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making significant financial decisions. Your situation is unique, and these general guidelines may need to be adjusted to your specific circumstances.