Zero-Based Budgeting for Beginners: The Simple Setup (No Spreadsheets Required)

If you’ve ever checked your bank account and thought, “Wait… where did my money go?” you’re not alone.

A lot of people try budgeting and quit because it feels too complicated, too strict, or too “finance-y.” The good news: zero-based budgeting for beginners can be simple, flexible, and realistic—even if you hate spreadsheets.

This guide will show you a zero based budget for beginners using nothing more than your phone’s Notes app (or a small notebook). You’ll also get a few real examples for different income levels, plus an easy way to handle irregular paychecks.

Before we start, here’s the plain-English definition.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

What a Zero-Based Budget Means (In Plain English)

A zero-based budget just means:

You give every dollar a job before the month starts—bills, groceries, gas, savings, debt, and even fun—so there’s nothing “unassigned” floating around.

That’s why it’s called “zero-based.” Not because you’re broke. Not because you spend everything. It simply means:

Income – expenses = $0 assigned (on purpose).

Example (super simple):

- You bring home $3,000 this month.

- You assign:

- $1,500 to housing + utilities

- $500 to groceries

- $200 to gas

- $300 to debt

- $200 to savings

- $300 to “life stuff” (kids, haircuts, random needs)

- Total assigned = $3,000

Now your budget “zeros out” because every dollar has a job.

Related Article

Start here to learn more about budgeting basics.

The Simple Zero-Based Budget Setup (No Spreadsheet Needed)

You can do this in:

- Notes app

- Google Keep

- A cheap notebook

- A whiteboard on your fridge

The tool doesn’t matter. The habit matters.

Step 1: Pick your budget timeframe (start with monthly)

Most bills are monthly, so monthly is easiest. If you get paid weekly or biweekly, we’ll handle that in a later section.

Step 2: Write down your “money coming in”

Use your take-home pay (what actually hits your account).

Include:

- Paychecks

- Side hustle income

- Child support/alimony (if applicable)

- Any consistent extra income

If your income changes month to month, don’t stress—use a conservative estimate (your “safe number”).

Step 3: List your “must-pay” bills first

These are the bills that keep life stable:

- Rent/mortgage

- Utilities

- Insurance

- Minimum debt payments

- Phone/internet

- Childcare

Tip: If you don’t know exact numbers, pull up last month’s bank transactions and copy them over.

Step 4: Add your “daily life” categories

These are the categories that usually blow up budgets because they’re easy to underestimate:

- Groceries

- Gas/transportation

- Eating out

- Household supplies

- Kids’ needs

- Medical/pharmacy

- Pet expenses

Step 5: Add “future you” categories (even if it’s small)

This is where people think budgeting is “not for them.” But saving doesn’t have to be huge to matter.

Add:

- Emergency fund (even $10–$25 is a win)

- Sinking funds (small savings buckets for predictable expenses)

Sinking fund examples:

- Car repairs

- Holidays

- Birthdays

- Back-to-school

- Annual insurance premiums

Step 6: Assign the remaining dollars to something on purpose

If you have money left after bills and basics, don’t leave it unassigned. Give it a job:

- Extra debt payoff

- Extra savings

- Fun money

- Home projects

- Health goals (gym, supplements, etc.)

And if you’re short? That’s not failure—that’s clarity. Now you can adjust before the month punches you in the face.

A Real Zero-Based Budget Example (Low, Medium, Higher Income)

Below are examples so you can see how this works for different income levels. These are not “perfect” budgets—just realistic starting points.

Example A: $2,400/month take-home (tight month)

- Rent: $1,100

- Utilities: $180

- Phone/Internet: $120

- Insurance: $150

- Groceries: $350

- Gas/transport: $160

- Minimum debt payments: $200

- Household/kids/personal: $90

- Emergency fund: $25

- Fun money: $25

Total = $2,400

Notice: small savings, small fun. Still counts. Still builds momentum.

Example B: $4,000/month take-home (more breathing room)

- Housing: $1,600

- Utilities: $250

- Phone/Internet: $150

- Insurance: $250

- Groceries: $600

- Gas/transport: $250

- Debt payments: $400

- Sinking funds: $200

- Emergency fund: $150

- Fun money: $150

Total = $4,000

Example C: $7,000/month take-home (higher income, same method)

- Housing: $2,400

- Utilities: $350

- Phone/Internet: $200

- Insurance: $450

- Groceries: $900

- Gas/transport: $450

- Debt payments: $800

- Investing/savings: $900

- Sinking funds: $350

- Fun/travel: $200

Total = $7,000

Same method. Different numbers. That’s why zero-based budgeting steps work for “all walks of life.”

Zero-Based Budget Categories to Start With (So You Don’t Overthink It)

If you’re new, start with 10–12 categories max. Too many categories = burnout.

Here’s a clean starter list:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Debt minimums

- Household/personal

- Medical

- Sinking funds

- Emergency fund

- Fun money

- Giving (optional)

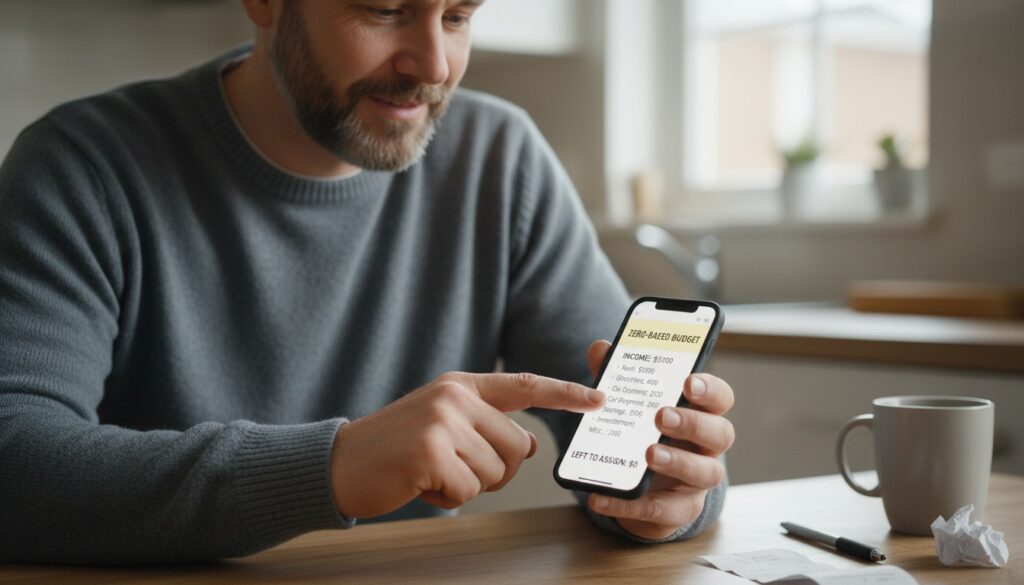

Budgeting Without Spreadsheets: The “Notes App Method” (Fast + Simple)

Open a note and format it like this:

Income: $____

Bills

- Rent:

- Utilities:

- Phone:

- Insurance:

- Debt minimums:

Living

- Groceries:

- Gas:

- Household:

- Medical:

Future

- Emergency fund:

- Sinking funds:

Fun

- Fun money:

Left to assign: $____Every time you add a category, subtract it from “Left to assign” until it hits $0.

That’s your zero-based budget method in its simplest form.

If Your Income Changes Week to Week (Do This Instead)

If you’re hourly, commission-based, or gig-based, use a “bare-bones first” approach:

- Start with your lowest expected income for the month.

- Fund the essentials first (housing, utilities, groceries, gas).

- When extra income comes in, assign it immediately:

- Catch up bills

- Add groceries/gas buffer

- Add sinking funds

- Add debt payoff

- Add savings

This is basically paycheck budgeting layered onto a zero-based budget.

Common Beginner Mistakes (And Easy Fixes)

Mistake 1

Forgetting “random life” expenses

Fix: Add a category called Life Stuff ($50–$200 depending on your situation).

Mistake 2

Making the budget too strict

Fix: Add fun money—even $10. A budget you can stick to beats a perfect budget you quit.

Mistake 3

Not checking in during the month

Fix: Do a 3-minute check twice a week. That’s it.

Simple Tools That Make This Easier (Optional)

You don’t need fancy tools to make a zero based budget for beginners work. But a few simple items can make it easier to stick with—especially if you’re trying to stop overspending in categories like groceries and eating out.

1) Cash envelope system (great for groceries/gas overspending)

If you tend to overspend with a card, cash envelopes can help because you can literally see what’s left.

2) Budget planner notebook (for people who hate apps)

If writing things down helps you stay consistent, a simple budget notebook can be a game-changer.

3) Receipt organizer / accordion folder (helpful for variable expenses)

Helpful if you’re tracking reimbursements, side hustle expenses, or just want less “paper chaos.”

4) Small home safe or lockbox (if doing cash envelopes at home)

Optional, but useful if you keep cash at home and want it secure.

Quick FAQ: “Is zero-based budgeting the same as living on zero?”

No. You’re not trying to end the month with nothing. You’re trying to end the month with no unplanned dollars.

You can assign money to savings, investing, and fun. The “zero” is just the math after everything has a job.

Your 15-Minute Action Plan (Start Today)

- Open your Notes app.

- Write your monthly take-home income.

- List your must-pay bills.

- Add groceries + gas.

- Add one small savings category ($10–$25).

- Assign the rest until “Left to assign” hits $0.

That’s it. That’s a zero based budget for beginners you can actually stick with.

Final Thoughts

If you’ve been avoiding budgeting because it felt confusing, restrictive, or “not for people like me,” let this be your reset. A zero based budget for beginners isn’t about being perfect—it’s about being intentional. When every dollar has a job, you stop guessing, you stop reacting, and you start making calm decisions ahead of time (even if your income is tight or your schedule is crazy).

Keep it simple: use the Notes app method, start with a handful of categories, and focus on the next small win—not the whole year. Your first month might feel a little messy, and that’s normal. The goal is progress: adjust your numbers, learn your patterns, and make the budget fit your real life instead of forcing your life to fit a “perfect” budget.

Most importantly, don’t wait until you “make more money” to start. Zero-based budgeting works at any income level because it gives you clarity and control right now. Start today with 15 minutes, assign your dollars, and then do two quick check-ins each week. That’s how this turns from a one-time attempt into a habit that actually builds breathing room.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Important Note: The information provided in this article is for educational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making significant financial decisions. Your situation is unique, and these general guidelines may need to be adjusted to your specific circumstances.