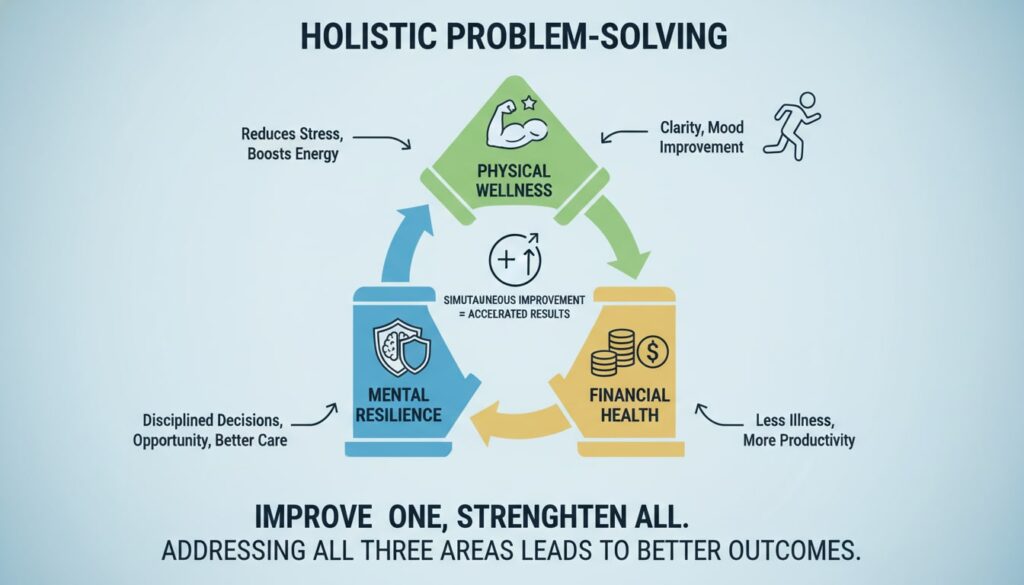

The Holistic Problem Solver: Connecting Mental, Physical, and Financial Solutions

You’re sitting at your kitchen table at midnight, calculator in one hand, stress ball in the other. Your back hurts from skipping the gym all week. Your mind is racing about that investment decision. And you’re wondering why everything feels so damn hard right now.

Here’s what most guys don’t realize: these problems aren’t separate. They’re connected. And once you understand how they work together, solving them becomes a whole lot easier.

“The journey of a thousand miles begins with a single step.”

– Lao Tzu

Ever notice how when one thing goes wrong, everything else seems to fall apart too? That’s because the different parts of your life—your health, your mindset, and your money—are all connected. When you’re stressed about bills, you might skip the gym. When you’re exhausted from poor sleep, you might make impulsive purchases. Understanding these connections is the key to solving problems that actually stick.

Let’s explore how mental resilience, physical wellness, and financial decisions work together to create a comprehensive problem-solving approach that works for real life.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

The Mind-Body-Wealth Connection

Your mental state significantly impacts your financial decisions. (Check out The Triangle of Well-Being: How Health, Mind, and Money Connect for the complete framework.) When you’re stressed or mentally exhausted, your ability to make sound financial choices takes a nosedive. Similarly, poor physical health can cloud your judgment and drain your mental energy.

Think of it like this: these three areas of your life aren’t separate rooms in a house—they’re more like a three-legged stool. If one leg is wobbly, the whole thing tips over. Let’s break down how these elements work together.

Mental Resilience: Your Financial Decision-Making Foundation

Here’s something interesting: research shows that when your head is clear, you make way better money decisions. Makes sense, right? You’re not going to invest wisely when you’re stressed and exhausted.

When you’re mentally resilient (meaning you can handle stress and bounce back from setbacks), you’re:

Better at long-term thinking instead of panic decisions

You know that feeling when you’re stressed and suddenly that impulse purchase seems like a great idea? Or when you’re anxious and you pull all your money out of investments at the worst possible time? That’s stress hijacking your decision-making. When your mind is clear and calm, you can think past today’s panic and focus on what actually matters for your future.

More disciplined with spending and saving

Mental clarity gives you the willpower to stick to your budget and financial goals. It’s not about being perfect—it’s about having the mental space to pause before swiping that card and ask, “Do I really need this, or am I just stressed?”

Capable of handling financial setbacks without spiraling

Life throws curveballs. Unexpected car repairs. Medical bills. Job changes. When you’re mentally resilient, these setbacks are problems to solve, not catastrophes that destroy you. You can think clearly about solutions instead of drowning in worry.

Want to build that mental foundation? Check out Building Mental Foundations After 40: The 3-Step Clarity Framework That Actually Works for practical strategies.

The Five Minute Journal

Physical Wellness: Your Mental Clarity Catalyst

Ever notice how after a good workout, problems that seemed impossible suddenly have solutions? That’s not coincidence. Your body and brain are connected—when one works better, so does the other.

Your physical health directly influences your mental sharpness. Consider these connections:

Regular exercise reduces stress hormones and improves decision-making

When you move your body, your brain releases chemicals that literally make you feel better and think clearer. A 20-minute walk can reduce cortisol (your stress hormone) and boost endorphins (your feel-good chemicals). This isn’t woo-woo stuff—it’s basic biology. And clearer thinking means better decisions about everything, including money.

Quality sleep enhances cognitive function and emotional control

You know how everything seems worse when you’re exhausted? That’s because lack of sleep impairs the part of your brain that handles rational thinking and emotional regulation. When you’re well-rested, you’re less likely to make emotional financial decisions or snap at people you care about.

Proper nutrition stabilizes mood and energy levels

Your brain runs on fuel, just like your car. Feed it junk, and it runs like junk. Feed it quality nutrition, and it performs better. Stable blood sugar means stable mood and energy, which means you’re not making desperate decisions because you’re hangry or crashing from a sugar high.

If you’re ready to address physical barriers, read Overcoming Common Fitness Barriers After 40: Your Blueprint for Success for realistic strategies that actually work.

Budget-conscious fitness options:

- Tight budget: You don’t need a gym membership. Walking is free, bodyweight exercises cost nothing, and YouTube has thousands of free workout videos. Check out a simple resistance band set for under $15—it’s like having a portable gym.

- Moderate budget: A basic gym membership ($20-40/month) gives you equipment variety and routine. Planet Fitness and similar gyms offer judgment-free environments perfect for guys just getting started.

- Flexible budget: Consider a personal trainer for 2-3 sessions to learn proper form, then continue on your own. Or invest in quality home equipment like adjustable dumbbells.

Sleep support: If sleep is your struggle, the book Why We Sleep by Matthew Walker is a game-changer. It explains exactly why sleep matters and how to improve it. For practical help, a simple white noise machine (around $50) can dramatically improve sleep quality.

For a complete physical reset, dive into The Over-40 Body Reset: A Guide to Sustainable Fitness.

Gaiam 3-in-1 Resistance Band Kit

Creating Synergy Between All Three Pillars

Now here’s where it gets powerful. Think of synergy like this: one person can push a car, but three people working together can push it much faster and easier. That’s what happens when you work on your fitness, mindset, and finances at the same time—each one makes the others easier.

The magic happens when you align all three aspects. Here’s how they work together:

1. Morning Exercise → Mental Clarity → Better Financial Planning

Start your day with 20-30 minutes of movement. It doesn’t have to be intense—a walk, some stretching, light bodyweight exercises. This physical activity clears your head, reduces stress, and gets your brain firing on all cylinders. Then, while your mind is clear, spend 10 minutes reviewing your finances, planning your budget, or researching that side hustle you’ve been thinking about.

See the connection? The physical movement creates the mental clarity that enables better financial thinking. You’re not trying to make money decisions when you’re foggy and stressed—you’re doing it when you’re sharp and focused.

2. Stress Management → Improved Health → Wiser Money Choices

When you manage stress effectively (through meditation, journaling, breathing exercises, or talking to someone), your body stops being in constant fight-or-flight mode. This means better sleep, lower blood pressure, less tension in your muscles. And when your body feels better, you make better decisions about everything—including money.

Chronic stress makes you reach for quick fixes: fast food, impulse purchases, get-rich-quick schemes. Managed stress lets you think clearly and make choices aligned with your actual goals.

Learn practical stress management techniques in Stress Management for Busy Men: Practical Techniques.

Stress management tool: The Calm app offers guided meditations starting at just 3 minutes. Or grab The Relaxation and Stress Reduction Workbook for under $25—it’s packed with practical techniques you can use immediately.

3. Financial Security → Reduced Stress → Better Physical Health

This one works in reverse too. When you have even a small emergency fund (start with $1,000), you stop living in constant financial panic. That reduced stress means you sleep better, your blood pressure drops, and you’re less likely to stress-eat or skip workouts because you’re too anxious to function.

Financial peace doesn’t mean being rich—it means having enough cushion that an unexpected $500 expense doesn’t destroy you. That peace of mind is priceless for your health.

For comprehensive financial strategies, check out The Mid-Life Wealth Building Blueprint: Your Path to Financial Freedom After 40.

The Relaxation and Stress Reduction Workbook

The Relaxation and Stress Reduction Workbook provides evidence-based techniques you can use year-round, not just during holidays.

Real-World Problem-Solving Examples

Let’s look at practical scenarios where this connected approach (working on all three areas together) makes a real difference:

Example 1: Career Transition at 47

Let’s say you’re considering a career change at 47. Your current job pays well but drains you mentally. You dread Monday mornings. You’re irritable with your family. And you’re scared to make a change.

Here’s how the three pillars connect:

- Mental: You’re stressed and second-guessing yourself daily. The negative self-talk is constant: “You’re too old.” “You can’t afford to start over.” “What if you fail?”

- Physical: Stress is causing tension headaches, poor sleep, and you’ve gained 15 pounds from stress-eating and skipping workouts.

- Financial: You’re afraid to leave steady income, even though you’re miserable. You haven’t saved much because you’ve been spending money to cope with the stress.

The holistic approach (meaning you tackle all three together):

- Physical action: Start walking 20 minutes daily to clear your head and reduce physical stress. This isn’t about weight loss—it’s about giving your brain space to think.

- Mental action: Use that walking time to think through your career options without pressure. No decisions, just exploration. Consider working with the What Color Is Your Parachute? 2024 guide to identify your strengths and interests.

- Financial action: Build a 3-month emergency fund so you feel financially secure enough to explore options. Even saving $100/month gets you started. Use a simple budgeting approach from The Total Money Makeover by Dave Ramsey.

- Integration: Notice how better sleep (from reduced stress and exercise) improves your decision-making about money. Notice how having some savings reduces your anxiety, which helps you sleep better and think clearer about career options.

See how each piece supports the others? That’s the power of working on all three at once. You’re not just changing jobs—you’re building a foundation that supports the change.

If you’re navigating a major life transition, read From Overwhelm to Clarity: A Strategic Approach to Life Transitions for a complete framework.

The Total Money Makeover: Classic Edition: A Proven Plan for Financial Fitness

Grab a copy of The Total Money Makeover by Dave Ramsey on Amazon. It's the bible of debt elimination and breaks down these concepts with even more real-world examples. Dave is a huge advocate of the snowball method and has helped millions get out of debt.

Example 2: Investment Decisions Under Pressure

You’ve got $5,000 saved, and you’re trying to decide whether to invest it, pay down debt, or keep it as emergency savings. You’re stressed about making the “wrong” choice, you’re not sleeping well, and you’re snapping at your family.

The connected problem: Your physical stress (poor sleep, tension) is creating mental fog, which makes the financial decision feel impossible, which creates more stress. It’s a cycle.

The holistic solution:

- Physical: Get one good night’s sleep before making any decision. Take a walk to clear your head. Your brain literally can’t process complex decisions when you’re exhausted.

- Mental: Write down your fears and concerns. Often, just getting them out of your head and onto paper reduces their power. Recognize that there’s no perfect answer—there’s just the best answer for your situation right now.

- Financial: Research your options when you’re calm and rested, not at 2 AM when everything feels like a crisis. Consider reading The Simple Path to Wealth by JL Collins for straightforward investment guidance.

- Integration: Make the decision from a place of clarity, not panic. Whatever you choose, you’ll be able to adjust later if needed. There’s no permanent mistake here.

Financial planning tools:

- Starting from scratch: If you’re living paycheck to paycheck, start by tracking where every dollar goes for one month. Just awareness is powerful. Use a simple notebook or the free version of apps like Mint or YNAB (You Need A Budget).

- Some savings: Focus on building a $1,000 emergency fund first, then work toward 3-6 months of expenses. Keep it in a high-yield savings account.

- Established finances: Consider diversifying with index funds or consulting a fee-only financial advisor. The Bogleheads’ Guide to Investing is excellent for DIY investors.

The Simple Path to Wealth: Your Road Map to Financial Independence and a Rich, Free Life

If you want to deepen your knowledge, grab, "The Simple Path to Wealth" by JL Collins. It breaks down money management for regular guys without the jargon.

The Holistic Problem-Solving Framework

Ready to apply this to your own life? Here’s a step-by-step framework you can use for any challenge you’re facing:

Step 1: Identify the Primary Challenge

What’s the biggest thing bothering you right now? Write it down. Be specific. Not “I’m stressed” but “I’m stressed about making $500 less per month than I need for bills.” That clarity matters.

Grab a simple journal or notebook—nothing fancy needed. Just somewhere to get thoughts out of your head and onto paper.

The act of writing forces you to clarify what’s actually wrong versus what feels wrong. Often, you’ll discover the real problem is different from what you thought.

Step 2: Assess Impact Across All Pillars

Now ask yourself how this challenge is affecting all three areas:

- Mental: How is this affecting my mood, sleep, and focus? Am I constantly worrying? Is it affecting my relationships?

- Physical: Am I stress-eating, skipping workouts, or feeling physically tense? Do I have headaches, stomach issues, or muscle pain?

- Financial: What’s the actual dollar impact, and what money fears am I dealing with? Is this costing me money directly, or indirectly through poor decisions?

Most guys discover their “money problem” is also causing physical symptoms and mental fog. Or their “health problem” is draining their bank account and causing relationship stress.

Understanding these connections helps you see the full picture instead of just treating symptoms.

Step 3: Develop Integrated Solutions

Create solutions that address multiple pillars at once. This is where the real power is—actions that create positive ripple effects across your whole life.

Instead of just “make more money,” try: “Take a 30-minute walk daily to clear my head, then spend 15 minutes researching side hustles.” The walk reduces stress (mental), improves health (physical), and the clear thinking helps you find income opportunities (financial).

Instead of just “lose weight,” try: “Meal prep on Sundays (saves money), which reduces weekday stress (mental), and supports fitness goals (physical).” One action, three benefits.

Instead of just “reduce stress,” try: “Create a simple budget so I know exactly where I stand financially (reduces money anxiety), use the mental relief to sleep better (physical), and use better sleep to think clearly about solutions (mental).”

For meal prep ideas that save money and support health, check out any basic meal prep containers set (under $20) and The Meal Prep Manual for simple, guy-friendly recipes.

Step 4: Implement with Balance

Don’t try to overhaul everything at once. That’s how you burn out and quit. Pick ONE action for each pillar this week:

- Physical: Walk 3x this week for 20 minutes

- Mental: Journal for 5 minutes before bed

- Financial: Track spending for one week

That’s it. Three small actions. Small, consistent actions beat massive, unsustainable changes every time.

Think of it like compound interest—small deposits made consistently create massive results over time. You don’t need to be perfect. You just need to be consistent.

Check out The Power of Small Wins: Building Unstoppable Momentum to understand why this approach works so well.

Step 5: Monitor and Adjust

Check in weekly. What’s working? What’s not? This isn’t about perfection—it’s about progress.

If walking isn’t happening, maybe try morning stretches instead. Or if journaling feels like a chore, try voice memos on your phone. If tracking every expense is overwhelming, just track your three biggest spending categories.

Stay flexible. The goal is progress, not perfection. Life happens. You’ll miss days. That’s normal. Just get back to it the next day.

Consider doing a weekly review every Sunday. Spend 10 minutes asking:

- What went well this week?

- What was challenging?

- What one thing will I focus on next week?

For a complete weekly system, read Sunday Financial Review: Weekly Money Check-In System.

Atomic Habits: An Easy & Proven Way to Build Good Habits & Break Bad Ones

Atomic Habits by James Clear breaks down how tiny mindset changes compound into major transformations. It's written in plain English—no psychology degree needed.

Your 7-Day Holistic Reset Checklist

Ready to start? Here’s your action plan for the next seven days:

Physical Actions:

Mental Actions:

Financial Actions:

Integration Action:

Essential Tools to Support Your Journey

Here are practical, budget-friendly tools that support all three pillars:

Mental Clarity:

- Atomic Habits by James Clear – The best book on building sustainable habits ($15-20)

- Mindfulness for Beginners by Jon Kabat-Zinn – Simple, practical meditation guidance ($12-15)

Physical Wellness:

- Resistance bands set – Portable, versatile, under $15

- Foam roller – Amazing for recovery and mobility ($15-25)

- Blender bottle – Makes protein shakes and meal prep easier ($10)

Financial Independence:

- The Total Money Makeover by Dave Ramsey – Straightforward debt elimination plan ($15-20)

- The Simple Path to Wealth by JL Collins – Best beginner investing guide ($15-20)

- Budget planner notebook – If you prefer paper over apps ($20-25)

Integration:

- The 5 AM Club by Robin Sharma – Morning routine framework that addresses all three pillars ($15-20)

Final Thoughts

Look, nobody’s expecting you to become a fitness guru, meditation master, and financial wizard overnight. That’s not realistic, and it’s not necessary.

What matters is understanding that these three parts of your life work together. Fix one, and the others get easier. Ignore one, and the others suffer.

You don’t need perfect balance. You just need to recognize the connections and work with them instead of against them.

“The journey of a thousand miles begins with a single step.”

– Lao Tzu

Start small. Pick one thing from each pillar this week. Walk for 20 minutes. Write down what’s stressing you. Check your bank balance. That’s it. Those three simple actions will show you how everything connects.

Remember, true success comes from understanding and nurturing the connections between your mental resilience, physical wellness, and financial health. By approaching challenges holistically (meaning you look at the whole picture, not just one piece), you’re not just solving problems—you’re creating a sustainable system for long-term success.

You’ve got this. And remember—it’s never too late to start connecting the dots.

Ready to dive deeper? Check out these related guides:

- Balance Fitness, Mindset & Money at 40: Your Simple Guide

- Energy Management for Men Over 40: Master Your Life

- Mindset Mastery: Why Most Men Stay Stuck (And How to Break Free)

- Finding Your Purpose After 40: It’s Not Too Late to Follow Your Dreams

Know a guy who needs to hear this? Share this article—sometimes we all need a reminder that we don’t have to tackle everything alone.

Disclosure

This article contains affiliate links. If you choose to make a purchase through these links, we may earn a commission at no additional cost to you.

Important note: The information provided in this post is for educational and informational purposes only. While we’ve spent over a decade studying health, wellness, and financial strategies, we are not a licensed healthcare provider, mental health professional, or financial advisor. Everyone’s situation is unique, so what works for one person might not work for another. For physical health matters, always consult your doctor before starting any new fitness program. For mental health concerns, please seek qualified mental health professionals. For financial decisions, consult with certified financial advisors who can assess your specific situation. The content here reflects personal research and experience but shouldn’t replace professional advice in any of these areas. By reading and using this information, you’re taking responsibility for your own decisions. Your health, mind, and money deserve professional guidance when needed. Stay awesome!